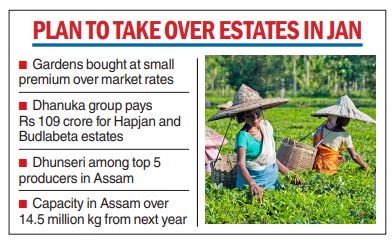

Chandra Kumar Dhanuka’s Dhunseri Tea is going to acquire two estates from Apeejay Tea Ltd to emerge as one of the top five producers in Assam.

Dhunseri is offering to pay Rs 109 crore for the gardens — Hapjan and Budlabeta — which are capable of producing 3.1 million kg annually at a valuation of Rs 350 a kg.

With a string of acquisitions lately — Dhunseri picked up three graders from Warren Tea last month — the Dhanuka-led group will have over 14.5 million kg of own production from Assam from next year, more than doubling throughput.

“They are two top-quality gardens and I am happy to reach an understanding with Apeejay. We are expecting to take over the assets from the middle of January 2023,” Dhanuka said.

Dhunseri is paying a little premium over the prevailing market rate to acquire the estates which are large and of good quality. One of the estates only produces orthodox tea which fetches higher prices in the export market.

While the listed company, Dhunseri Tea and Industries, is going to have 13 million kg of its own tea, group entity Madhuting, owned by Dhanuka’s daughter, has about 1.6 million kg under its fold. Dhunseri also processes about 3.5 million kg of bought leaf from third parties.

Moreover, the Dhunseri group have plantations in the central African country Malawi where 9 million kg is produced, apart from 4 lakh kg of macadamia nuts.

Asked if he is looking for more assets, Dhanuka claimed his ‘‘appetite is full for now’’ as he wants to avoid borrowing from banks to fund any deal. “I don’t want to leverage the balance sheet,” he added. Many tea companies are under stress due to the incidence of high debt in an environment of low operating profit margins.

Dhanuka’s acquisitions are a contrarian bet given that estate owners often complain of oversupply of leaf from small growers keeping prices under pressure with cost rising because of an increase in wages and costs of agricultural inputs. At a time margins are squeezed, having little debt, except working capital, may go a long way to make the operation sustainable.

“Tea may be profitable if managed well, but more profitable with zero debt,” he said.

He also has the comfort of Dhunseri Group’s joint ownership of the petrochemical business in Haldia and Panipat with Indorama Group of Bangkok. Dhunseri is also setting up a packaging film unit at Panagarh for Rs 1,450 crore. Overall, the turnover of the group is over Rs 10,000 crore.