Dividend yield seems like an idea whose time has come. In a market characterised by bearish sentiments, driven largely by fears stemming from inflation and geopolitical factors, investors are increasingly taking to the idea of dividend yield. At the very centre of attention are stocks of companies that have consistently rewarded stakeholders — a bold strategy that can sustain risk-takers’ aspirations over the long term.

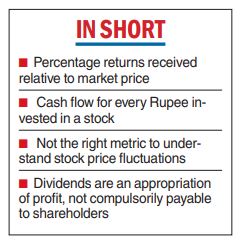

Dividend yield of a stock is the dividend per share paid annually divided by the market price. The metric has a unique appeal for shareholders; a stock with a superior dividend yield is coveted by the investor community. Companies that consistently pay good dividends are often singled out for their performance. Regular payouts are a welcome sign, regarded highly by investors who want more than just valuation growth. Rapidly advancing stock prices and regular dividend receipts together make a potent combination for market participants.

What prompts the latest inclination for high dividend payers is the overall sentiment — somewhat negative at this juncture — prevalent in the market.

Equities are not expected to do well in relative terms in the coming quarters, at least for the ensuing season. A clutch of reasons, ranging from higher interest rates (an end of cheap money for the corporate sector) to the run-up to the next general election, are being cited by investment circles. The emerging trend is not in favour of equity allocation, it is argued.

New allocators, however, may still pick up reliable names, including those that can potentially pay higher dividends. The latter, I should point out, are an appropriation of profits.

A company that has done well in terms of profitability is expected to suitably reward its shareholders.

Ergo, a series of regular payouts is often construed as a panacea in an erratic market.

Dividend yield strategy

Investors are expected to address the issue in two ways. First, those who allocate directly with the help of their brokers can invest in select good dividend yielding stocks. Second, those who for one reason or another, do not invest directly can identify good fund managers.

The latter tactic, which implies acquisition of units of dividend yield funds, is quite convenient to execute at the moment. One-time allocations, followed up by systematic investment plans, are both realistic solutions. It is not for me to suggest how exactly an investor should allocate — that should be a function of his risk-taking ability — but a gradual increase in exposure can be recommended.

Among the relatively high scorers are stocks of multi-nationals, commodity players, energy companies, financial services firms and so on. A number of these outfits have recorded handsome profits over the years, thanks to high productivity and smart margins. Profits have been retained to a marked extent too, which have enabled their managements to follow a well-articulated dividend payment policy.

Profitability metrics, incidentally, have also acted as triggers for the stocks. Valuations have accelerated on the bourses, leading to decent returns for investors. The latter, thus, have benefited on both fronts.

Challenges

The steepest challenges come in the shape of asset allocation and stock-picking. Not every stock is a good acquisition in so far as dividend payout is concerned. Some managements may not pursue a liberal reward policy, others may be willing to pay at a lower rate.

A correct approach is, therefore, necessary to construct a portfolio of high dividend yielding stocks. Strategies followed by some of the better performing funds can lead to vital clues.

A quick look at the current crop of dividend yield funds has thrown up interesting trends. These are, it may be mentioned, all essentially positioned as open-end, diversified equity funds that appeal to investors seeking capital appreciation. The USP in question is dividend yield, based on which their holdings are selected. There is no market capitalisation bias.

A review of the same underscores a medley of sectors — banking, information technology, manufacturing, consumption and commodities. Some of these, incidentally, are prominent constituents (in terms of weightages) of the main indices, Sensex and Nifty. A specific reference may be made to certain public sector undertakings, which have paid good dividends historically. I will not mention names in this context, but most of these companies are established players in their segments. They lead these fields in terms of turnover, production capacity, brand equity, geographical reach and profitability.

Caveat

Discerning investors may heed a warning or two. Working out a portfolio merely on the basis of a single theme (however powerful) is extremely difficult for the ordinary participant. It is important not to miss the woods for the trees. Ergo, the concept of dividend yield needs to be viewed as an enabler of sorts — one of several enablers, in fact.

An investor may instead apply his skills to build a diverse, well-rounded portfolio. Direct equity is an option for those who can manage it themselves. That requires time and abilities. Indirect investment with the help of professional fund managers is recommended for others. That should work well in a market as quirky as this.

The writer is director of Wishlist Capital Advisors