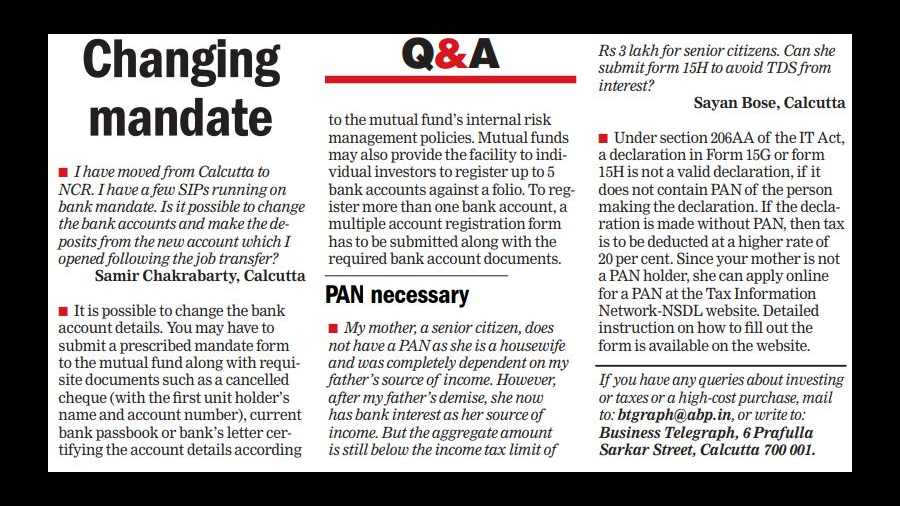

The transience of life applies equally to each one of us. Yet, for decades, not everyone has had equal means of financially securing their future. The case in point here is the eligibility of homemakers to obtain an independent term insurance policy for themselves.

For decades, one’s economic contribution has been linked solely to their financial output. Possibly this is why the contribution of homemakers has been vastly underestimated for a long time. This notion also played a part in them not being able to opt for an independent term insurance policy until recently. However, that changed with the recent launch of independent term plans for homemakers, which they can buy irrespective of their spouse’s policy or income status.

These products by insurance companies such Max Life, Tata AIA, IndiaFirst Life Insurance and HDFC Life marks a new dawn in the country’s financial protection landscape, especially for women. With enhanced accessibility to insurance, homemakers can cast their own safety net for their dependants without having to depend on their spouse. Here’s why it’s imperative for every homemaker to exercise better control over their finances.

Take your own decisions

Studies show that even after being equipped with financial means, women often don’t take charge of their financial planning. A recent survey by Women Investors Network found that about 48 per cent of women depend on men in the family for investment decisions. This dependence tends to be higher in the case of homemakers. Term insurance is as much of a necessity for a homemaker as for any earning member of the family. However, until now, they were dependent on their spouse to buy one, that too with certain conditions. Apart from this, they would only be covered for 50 per cent of the sum assured and the income multiplier would depend on the spouse’s annual income.

Suppose, if the annual income is Rs 5 lakh and the income multiplier is 15 times the annual income, then the husband would be eligible for a cover of Rs 75 lakh. Now, out of this if we assume that he takes a cover of Rs 50 lakh, that leaves the wife with a cover of Rs 25 lakh.

If the husband ends up taking a Rs 75 lakh cover, then the wife won’t be eligible for any cover. The rules of the policy were mainly decided by the earning spouse’s income and choice of cover. So, even if the homemaker had a policy, there was little under her control. With this plan, this dependence has been eliminated.

Ensuring financial equality

This independent policy is available for homemakers in the age bracket of 18-50 years. To ensure higher adoption, the plan has been designed in an inclusive and accessible way. There are two basic conditions that must be fulfilled by the policyholder — the household income should be a minimum of Rs 5 lakh annually, and the homemaker should be a graduate. Some policies also require the homemaker to have completed class 10 or 12. The earlier dependence on the spouse’s income or policy has completely been ruled out.

Homemakers’ contribution

While the contribution of a homemaker might not be tangible, it still accounts for a significant part of the family’s financial infrastructure. It’s important that she also has equitable access to a term insurance policy.

Women make up for 49 per cent of the total population in India. However, only about 16-20 per cent of them are part of the workforce. That leaves a fairly significant share of the female population who form a crucial pillar of the economy through unpaid work and care. Their absence impacts finances in ways more than one. Household chores and looking after family members make up about 39 per cent of the GDP according to data by UN Women.

Last year, the Supreme Court also emphasised that the common notion of homemakers not contributing to the economy is problematic and must be overcome. The unfortunate demise of a homemaker will lead to the restricted choice of job roles for the husband, or might even force the family to relocate or hire paid care for the children.

All of these raise the spending of a household substantially. While nothing can make up for the loss of her life, at least her dependants and their future can be secured financially. This change comes at a time the pandemic still continues to be a looming threat to the health and lives of millions.

This policy helps quantify the relevance of the socio-economic contribution made by homemakers. This is also a huge leap forward in the journey of financial inclusion, apart from the long-due recognition of unpaid work and care. However, this change will only be fruitful if more women realise the need for term insurance and take charge of their financial decisions.

(The writer is business head — term life insurance, Policybazaar.com)