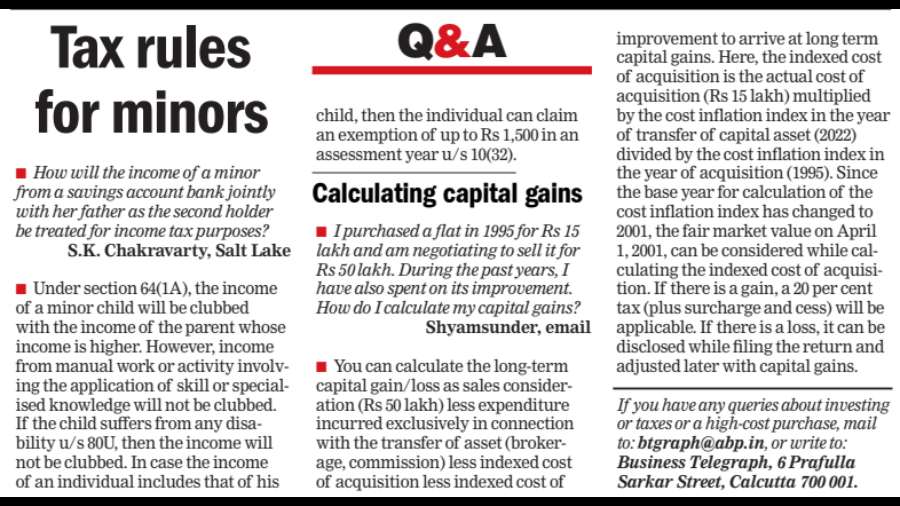

Digital lending has been in the news lately. The digital availability of credit is a huge step forward. It is central to the democratisation of banking and finance.

Digital lending is solving a historical challenge. Indians in the furthest reaches of this country didn’t have the advantage of being serviced by bank branches.

But thanks to advancements in regulation and technology, it is now possible for those Indians to pick up their phone, complete their KYC via video and Aadhaar, avoid the queues and the photocopies, and get their credit facility within a day. Video KYC especially is a ground-breaking innovation for which regulators need to be congratulated.

On the flip side, technology has also enabled some bad agents whose proliferation needed to be checked. Predatory interest rates, breach of data, unethical recovery practices, hawala transactions and non-compliant behaviour had become concerns that couldn’t be ignored.

Earlier this month, the RBI announced a new set of rules that digital lenders and their intermediaries must play by. The rules focus on the rights of customers. Here’s what you should know about them.

A look-up period for loans

Those savvy with personal finance would know there’s a free-look period for insurance products. If you buy a policy and it fails to meet your expectations, you can return it within a two-week window and claim a refund.

In a somewhat similar fashion, digital loans will now have a look-up or cooling period in which you could return your loan by paying back your principal with proportionate interest. Since interest needs to be paid, it’s not a free look-up.

However, this will protect consumers from situations where the terms and conditions of a loan disbursed to them are not to their expectations. Banks will need to create policies around this.

While the regulation applies to digitally disbursed loans, this is a customer-centric move that can be extended to offline loans as well.

Customer’s consent is key

The RBI has emphasised consent-based selling and servicing of lending products. We saw this earlier in the new rules on credit cards. We are seeing the same philosophy being applied to digital loans.

We have read media reports about some lenders collecting data such as the borrower’s phone book numbers and disturbing the borrower’s friends and family over late payments. These recovery practices are unethical.

The RBI has now said lenders do not have blanket consent to all data from the borrower’s phone. Lending apps must not access files, contact lists, or call logs. Any data collected by the lender must be need-based and only with the borrower’s consent.

More importantly, consent isn’t permanent. It can be given, denied, or revoked at a later stage. Lenders may also need to delete the data if the borrower so wishes.

Fact sheet to mention costs

The borrower will be provided with a one-page fact sheet which would mention the cost of the loan as an annual percentage rate.

This is similar to the new rule about credit cards which must also be issued with a one-pager. The rule is aimed at transparency.

Furthermore, in digital lending, you have the lender, the borrower, and an intermediary (a loan service provider) who aids the loan disbursal.

The RBI has made it clear that the intermediary cannot recover any service costs from the borrower. The costs can only be received from the lender.

BNPLs to report to bureaus

When you take a loan or credit card, your repayment record is reported to credit bureaus such as CIBIL and Experian. The bureaus use this information to compute your credit score.

Recently, we’ve had instances where some digitally disbursed Buy Now Pay Later loans weren’t reported to the bureaus. To a good borrower who is disciplined in repayment, this means not getting the benefit of a better credit score.

To check this, the RBI has now said all loans regardless of their tenor or nature, if sourced digitally, will have to be reported to the bureaus.

No rerouting of funds

With the new rules, the RBI has clarified that all payments — be it the disbursal of the loan or its repayment — need to happen directly between the borrower and the lender. Funds cannot be rerouted through other channels. The exception to this are instances of co-lending or specified use-cases permitted by the RBI.

Recently, it was highlighted in media reports that money was being rerouted by shell companies using hawala transactions. The new regulation is a positive for digital lending because it clamps down on non-compliant behaviour by some rogue lending applications.

India now has a pre-eminent position in digital payments, thanks to UPI. And thanks to progressive regulations, it is getting there in lending as well. Technological and regulatory innovation will help maintain India’s pre-eminence in fintech. These new rules will help not just consumers make better decisions but also weed out bad agents from the digital lending industry.

The writer is CEO, BankBazaar.com